.png)

There is a saying that economists are trying to predict oil price movements so that meteorologists do not feel ashamed of their work. However, there is a grain of truth in this joke. NES visiting professor Alexander Malanichev who has been studying commodity prices for 30 years, talks about forecasting methods, accuracy of forecasts and ways to improve it. Spoiler: the most important thing is to consider fundamental factors and to listen to the market signals.

Only God knows how much oil will cost in the future, people in the industry like to joke. Meanwhile, this is one of the key projected indicators for the global economy. Neither governments nor corporations can do without it, since the role of oil in the economy is just too great. So, the first step is to identify the main factors that make up the price.

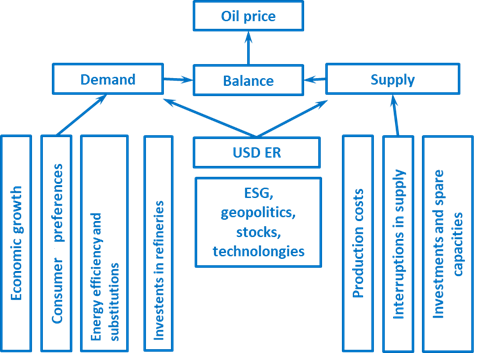

Roughly, they can be divided into two large groups: fundamental and non-fundamental. Fundamental factors usually imply the oil market balance, that is, the difference between production and consumption, as well as factors affecting them (the main ones, but not all of them are in Fig. 1). In the case of a production surplus, the difference is stored in the commercial and strategic stocks to be used in the case of shortage.

Non-fundamental factors include expectations of the stock market, which can be represented by the prices of oil futures and options. Expectations affect the market price, but not the physical market balance.

Fig.1 Key factors affecting the global oil market balance and the oil price

Source: composed by author

Oil consumption growth is driven by the dynamics of the world economy. Fears of a recession in developed countries, rising risks for developing countries or a slowdown in China's GDP may all cause a drop in oil consumption. Demand factors also include consumer preferences and competition between different types of fuels, e.g. transition to NGV fuel or electricity. Oil reserves, production cost, OPEC policy, etc. are among the major production factors.

Important factors affecting both consumption and production are government regulation, ESG policies, geopolitics (the Iran nuclear deal, Russian oil embargo and price cap, sanctions against Venezuela, etc.), the development of technologies on the production and consumption sides (green energy, electric vehicles, etc.). Another factor is the USD exchange rate: if the currency becomes more expensive, then the dollar-denominated oil prices decrease, and vice versa. However, the relevance of this factor has weakened recently.

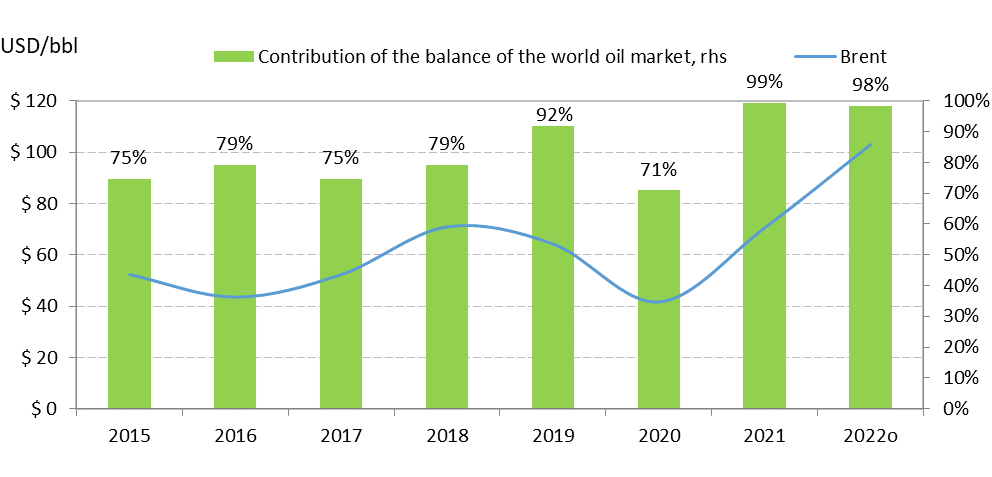

What factors have the largest impact? The analysis shows that since 2015, despite the aggravation of geopolitical and trade conflicts, fundamental factors account for 75-90% or even up to 100% of the changes in the average annual oil price (Fig. 2). The contribution of speculative factors decreased after 2014, when more than 5 mln barrels of US shale oil appeared on the market. This has made the global oil market more predictable, as fundamental factors are easier to forecast than market expectations.

Fig. 2. The contribution of fundamental factors to the price change

Source: EIA, author’s calculations

Forecasting methods can be conditionally divided into expert, analytical and market ones.

Consensus forecast is probably one of the best among expert methods, since averaging different individual outlooks eliminates the possibility of a random error. At the same time, there is a risk that a collective misconception will remain, but you can try to avoid it, for example, by using the method of the Delphic Oracle (or Delphi, for short). It allows to eliminate distortions of weak experts when discussing the forecasts. There are other ways to improve the quality of consensus, for example, by weighing the opinions of experts depending on the accuracy of their past forecasts.

In my courses, I conduct forecasting sessions 4-6 times a year and at every fifth session I get an absolutely accurate forecast using the Delphi method, despite the fact that none of the students hits the target. I still can't forget the delight of the directors of coal mines and processing plants from Kuzbass, who learned the power of the Delphi method in the walls of the Moscow State Mining University last summer.

The range of analytical approaches to forecasting oil prices is very wide and most of them use complex calculations, studying changes in prices of crude materials and derivatives, exchange rates, etc. Each of these methods is good on a particular forecasting horizon. However, many of them are formal, and it is often impossible to explain what market factors determined the forecast.

A reliable method of forecasting is finding out the opinion of the market itself. The price of oil is determined during trading on exchanges where there are enough players and liquidity to consider the oil market efficient most of the time. Therefore, one of the best ways to predict the price is a naive forecast, i.e. extrapolation of the current price (for example, the expected future average annual price is assumed to be equal to the current monthly average) or one based on futures prices.

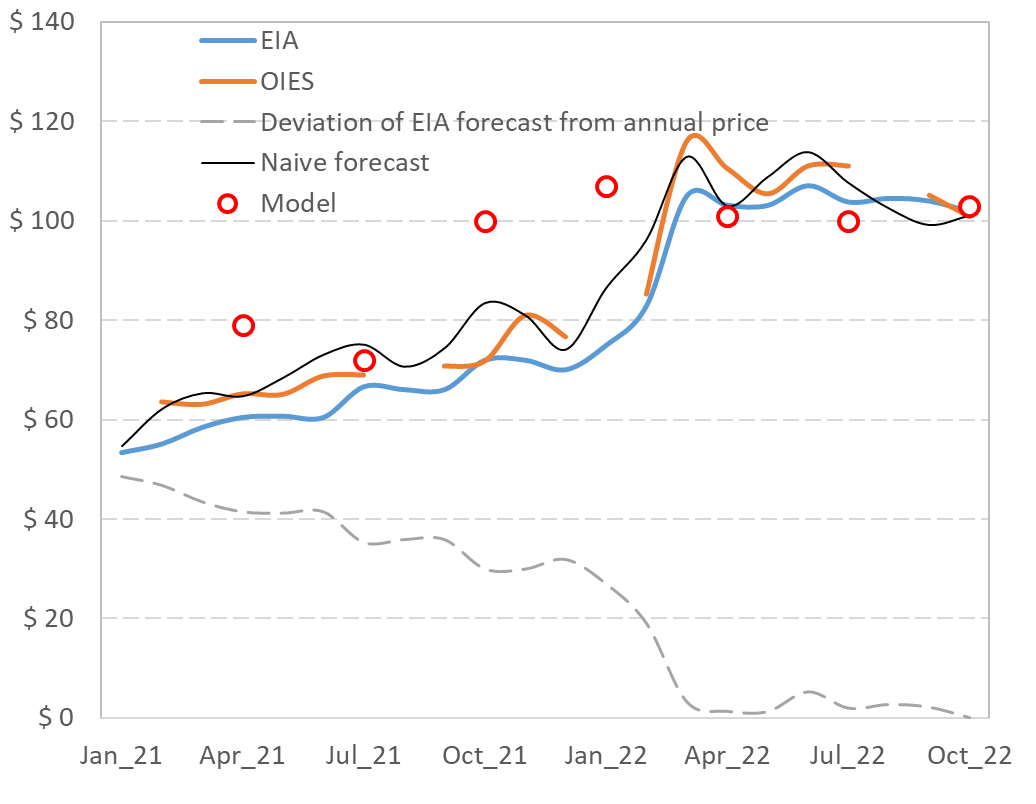

Data analysis shows that a naive forecast beats, for example, the forecast of the US Energy Information Administration (EIA STEO). Among the world's major "forecasters", it is the only one now that publishes monthly outlooks and provides fairly complete statistics on the global oil market. In Fig. 3, I compare different forecasts of the average annual spot price of Brent oil in 2022, made from January 2021 to October 2022. On the horizon of 15 months through the end of 2022 (the starting point is October, since at this period companies are drawing up their budgets), the EIA forecast error reached 42%, while for the naive forecast it was 21%.

If we take a wider horizon of 22 months, then only in three months the EIA forecast was more accurate than the naive one. The experts of the Oxford Institute for Energy Studies (OIES), who began issuing their monthly forecasts in 2021, also lost to the naive forecast – albeit with a smaller score. This clearly confirms the theory of the Nobel laureate in Economics Eugene Fama about the effectiveness of markets.

The cost of insurance against the rise or fall of the oil price in the form of the oil options can also tell about the market views. The most popular strike (the price of the underlying asset) of the call options for WTI oil on the 12-month horizon is now $120/bbl. That is, oil consumers are buying insurance against a sharp rise in prices due to an embargo on Russian supplies. But, the futures market does not believe in such a high price yet.

Options have performed well in forecasting prices even for this turbulent year. While in the middle of last year, the futures market expected for the end of 2022 the price of WTI crude oil at $61/bbl, the options market pointed to $100/bbl, which is not far from the current values. Options to buy oil at this price with an expiration date in December 2022 were the most popular on the New York Mercantile Exchange.

In June 2021, JP Morgan analysts considered such a forecast overstated and "almost impossible", although earlier in May they issued an almost accurate outlook for 2022 for Brent at $104/bbl. Meanwhile, already in November 2021, the investment bank significantly raised its forecast – to $125/bbl, so it overestimated the average annual price by 18%, assuming that OPEC+ would face a shortage of production capacity. In September, the bank predicted a price of $98/bbl for Q3 2022, which turned out to be close to the actual value of $101/bbl.

It should be recognized that forecasts in general tend to become more accurate as the horizon shrinks. Thus, it is like billiards: the closer the ball is to the pocket, the higher the probability of hitting it.

The quarterly forecast made using a model linking the price of oil and the balance of the global market, a key factor influencing the price in recent years (Fig. 3), was much more accurate on the horizon of 15 months (from October 2021 to December 2022). The deviation of the forecast value from the actual average annual price for 2022 does not exceed 4%.

Fig. 3. Evolution of forecasts of the average annual oil price (Brent) in 2022 and their accuracy (deviations from the actual price) depending on the month of the forecast release

Source: EIA, OIES, author’s calculations

I forecast global market balance (consumption and production) based on the monthly EIA data, which, oddly enough and according to my calculations, is not too consistent even with its own forecasts of oil prices. I also use additional key supply factors in the model: OPEC+ decisions, US shale oil production, and forecasts of other organizations.

Deviation of forecast from actual data can originate from:

unaccounted non-fundamental factors (their role is minimal for 2022, see Fig. 2); and

inaccuracies in forecasts of global oil production and consumption. However, these EIA forecasts are quite accurate: since January 2021, the expected average annual oil production and consumption in 2022 have deviated from the fact by a maximum of 1.9% and 1.8%, respectively.

In addition to higher accuracy and a simple explanation of the result, the advantage of the model approach is the applicability of the What-If Analysis. You can check the probability of the realization of marginal forecasts of other experts or market participants; assess the impact of decisions to reduce production (voluntarily or as a result of an embargo) or to lift sanctions against Iran, as well as to release oil from US strategic reserves; etc.

For example, the model allows us to analyze what impact the refilling of US oil reserves can have on the market, which, according to President Joe Biden, will begin only when the price drops to $67-72/bbl. It means that at this level, the supply of 1 mln bbl/day to the market from America's Strategic Petroleum Reserve (SPR) will be replaced by approximately the same amount of consumption, and the balance of the global oil market will shift by 2% towards a deficit. But as soon as the refilling of stocks begins, information about this will instantly lead, according to my estimates, to a 5-10% price increase. It will again exceed the threshold of $70/bbl and the refilling of the SPR will stop. In other words, in order for the replenishment of stocks to be sustainable, the price must fall significantly below $70/bbl.

Conclusions

Fundamental factors have been playing a major role in oil price changes since 2015. Therefore, forecasting consumption and production is most important.

The model linking the global market balance and the price of oil provides for a more accurate forecast.

The model is a convenient tool for applied What-If Analysis.

Do not forget to listen to the market!